on MLP AG (ETR:MLP)

MLP SE's Solid Q1 Performance Prompts Buy Recommendation

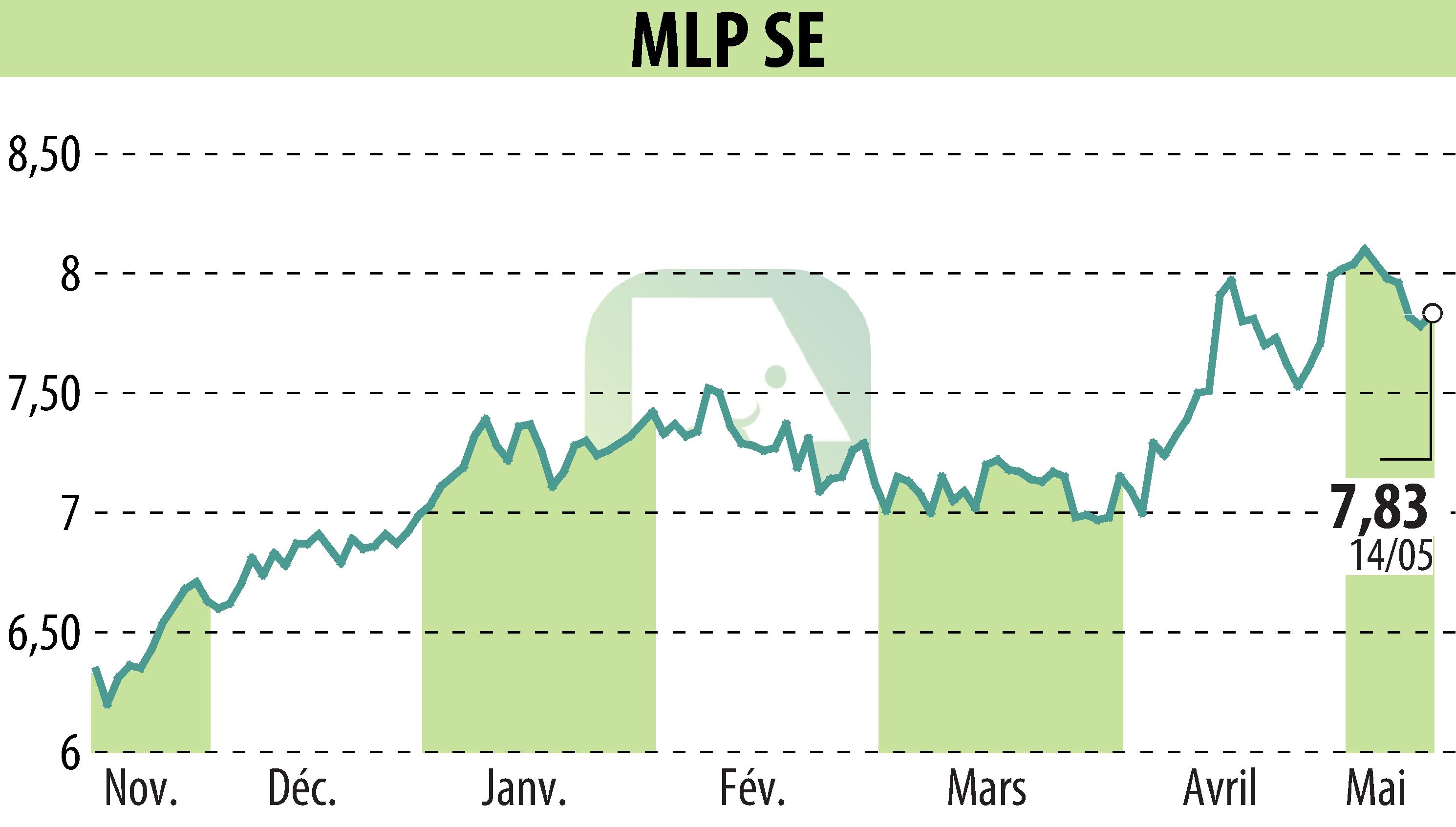

MLP SE has reported strong first-quarter results for 2026, prompting NuWays AG to maintain a "Buy" recommendation with a target price of €12. The company's total revenues increased by 4.7% year-over-year to €315 million, driven by improvements across all divisions. This growth led to a 10.2% increase in EBIT, reaching €41.3 million.

Wealth management showed resilience despite volatile market conditions, with revenues rising to €97.6 million, supported by a higher assets under management base. Life & Health remained stable, while Property & Casualty revenue grew by 11.7% to €114 million, bolstered by inflation-linked premium adjustments and AI-supported claims handling.

MLP maintains its EBIT guidance of €100-110 million for the full year, with slight revenue growth expected across all sectors. The company offers a 5% dividend yield and anticipates a CAGR of approximately 14% in adjusted EBIT through 2028.

R. E.

Copyright © 2026 FinanzWire, all reproduction and representation rights reserved.

Disclaimer: although drawn from the best sources, the information and analyzes disseminated by FinanzWire are provided for informational purposes only and in no way constitute an incentive to take a position on the financial markets.

Click here to consult the press release on which this article is based

See all MLP AG news